What if Constellation Software pivoted to sub shops, sand, and socks? What if a programmatic acquisition strategy had no underlying business logic or synergies? What if we invented self-funded search from first principles and took it public? What if the 2021-vintage SPACs never really went away? Teamshares is attempting to answer these very important questions.

Search funds / entrepreneurship through acquisition is probably the fastest growing path for top MBAs and is gaining traction with mid-career executives. Even the New York Times is on it (and has been for over a decade – early Chenmark spotting!). I’m (maybe obviously) a believer in the search fund model. My day job is helping to run a company acquired through the model, I used to work for a large search investor and I continue to put my own money in these kinds of opportunities. It’s an awesome ecosystem – but that’s not quite what we’re here to talk about.

VC-backed companies are sometimes criticized for re-inventing business models that already exist, but at wildly different valuations (see WeWork’s $47 billion peak valuation and revenue multiple of 15x vs. Regus at 1-2x). In Teamshares, some “tier one” VCs including Khosla Ventures, Spark Capital and Union Square Ventures have effectively backed a search fund-like consolidation vehicle, convinced themselves it’s an appropriate VC investment, and funded nearly $250 million of equity capital. They call it fintech on their websites. And they’re now trying to take it public through a SPAC, which have more than a bit of earned stigma around business quality.

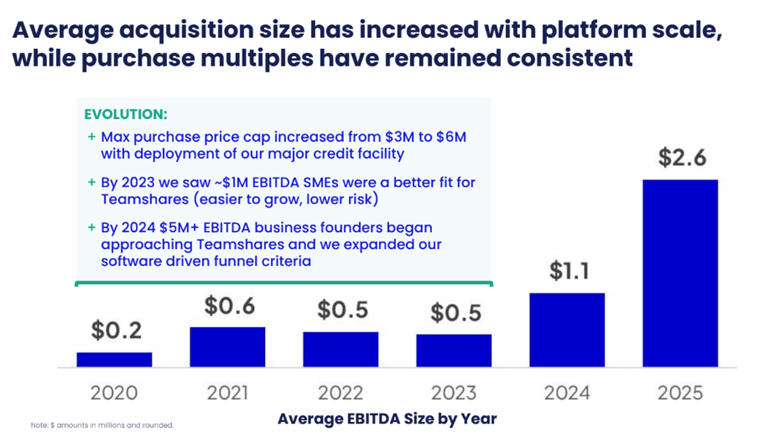

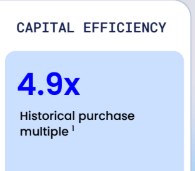

Self-funded search is a flavor of search fund, where the entrepreneur doesn’t raise investor capital while they’re looking for an acquisition (hence the name self-funded). These deals are smaller “traditional” search deals, typically under $2 million EBITDA. They often have a highly levered capital structure, i.e. ~80% leverage between SBA debt and seller debt, and are almost always acquired for under 5x EBITDA. Teamshares is buying similarly sized companies for about 5x, and debt-financing most of the purchase price. The playbook is eerily familiar, and if you added up the companies in a large search investor or SMB-oriented PE investors’ portfolio, the scale would be about the same too. But that portfolio wouldn’t get valued at a giant write-up, just because there are a lot of companies in the portfolio.

Teamshares is walking a really fine line in its marketing between talking about Main Street businesses like a noble profession and a piece of financial data. As an aside – the PE guy who uses “asset” is way more offensive than talking about a “deal” – these businesses are often someone’s life work and I guarantee they don’t think about them as an “asset”.

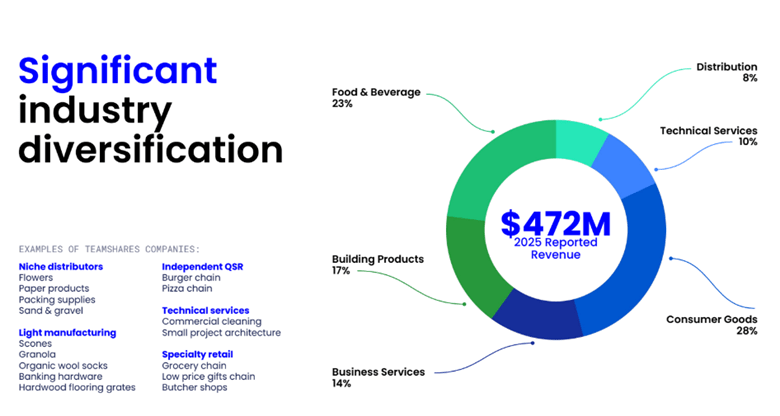

The SPAC presentation shows sector mix, and a few companies are discussed. It’s roughly half food and beverage (i.e. restaurants and grocery stores) and consumer – not exactly the places where most search fund entrepreneurs are playing, because these businesses are hard to operate at small scale for first-timers, and also hard to scale. The joke about becoming a millionaire – start with a billion dollars and buy an airline – applies to these businesses too; restaurants and specialty retail have among the highest failure rates of any category of small business. Let’s assume that the rest of the verticals are similar quality to self-funded search companies, which seems reasonable based on the examples below. That would suggest that half the companies Teamshares bought were probably not investable by self-funded search entrepreneurs. Given their median multiple is 5x EBITDA versus nearly all self-funded transactions happening under 5x EBITDA, they overpaid for the other half.

Teamshares’ Series D press release calls out a dozen businesses – some, such as an auto service business in Western Massachusetts, and a residential plumber in Waco, Texas, are in sectors where there are many PE rollups, some documented synergies and logic to scale. But Teamshares doesn’t appear to be pursuing synergies or consolidation within sectors – they’re purely aggregating EBITDA. Some of their acquisitions are in sectors most self-funded searchers wouldn’t touch – too discretionary and difficult to run. A retail bakery in Tennessee and a camera store in Fresno come to mind. Perhaps the LOI win rate is so high because no one else wants to pay 5x EBITDA for these businesses. Putting a public company wrapper and business intelligence layer on a portfolio of unrelated SMBs doesn’t warrant seven turns of multiple expansion.

Hilariously, they have the gall to call themselves “thesis driven” as a way to distinguish between them and other programmatic acquirers. If anyone thinks the Teamshares thesis of “baby boomers own businesses and want to retire” is way more unified than, say, Heico or Transdigm’s thesis around aerospace, please let me know what Polymarket bets you’re making, and even though I’m not a betting man, I’ll take the other side.

There’s a lot of discussion in the SPAC presentation and transcript around equity efficiency, compounding, and using free cash flow to fund acquisitions. All makes sense – except for the discussion around employee ownership that’s all over their seller pitch, public facing website, and even shows up on some of their operating division websites.

Teamshares has a stated goal of enabling its companies to become 80% employee-owned over 20 years. That means that less of the future cash flow from these acquisitions will go to Teamshares and its shareholders over time to fund acquisitions. Valuations are reflections of estimates of future cash flows, and this bucket is slowly leaking, so the M&A flywheel has to run faster every year, or the valuation will crash. More precisely – if ownership is majority-transitioned to employees over time, there’s limited terminal value in any underlying subsidiary. The lack of discussion of the major equity dilution coming to proposed public investors reads like an intentional oversight and an obvious flaw in the business model.

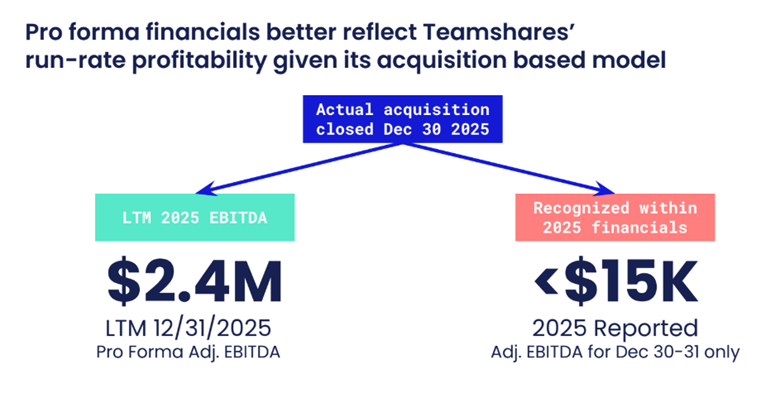

A SPAC transaction is 100% necessary for a company like Teamshares to go public – SPACs can adjust EBITDA and use projections to present their information in ways that wouldn’t work in a normal IPO prospectus. Teamshares is targeting a 11.9x pro forma multiple (i.e. 12 months of Adjusted EBITDA credit for recent acquisitions). And while I don’t think leaning on “pro forma” in the example below is unreasonable, it’s also rare in the public company context.

This slide doesn’t exist in a normal IPO prospectus, and public company investors typically don’t give credit for Pro Forma EBITDA.

There’s also a belief within private equity that roll-ups will struggle as public companies because public equity investors don’t give “pro forma” EBITDA credit for acquisitions. Pro forma EBITDA isn’t a metric that shows up prominently in a 10-k. More broadly, there’s an interesting intellectual capital allocation question around consolidations that Teamshares is unwittingly helping to solve. Consolidations operate on multiple arbitrage – you buy a tuck-in for 7x EBITDA in a platform that trades for 12x EBITDA. Value creation. It’s been the model in many corners of healthcare services, for example. The diversification benefit that Teamshares talks about is also present – instead of being tied to a single office and a few practitioners, the acquisition is suddenly one of a hundred, and in total, company performance is more predictable than individual office performance. A doctor going out on leave in a $1m EBITDA single office practice can hugely impact EBITDA, whereas it might not be noticed in the $100m EBITDA platform. But part of the logic is also that the individual practice will get the benefit of resources through the platform. It could be marketing benefits, purchasing synergies, etc. – things that will make office earnings go up faster because they’re part of the platform. That hasn’t always occurred (many 2019-2021 era healthcare roll-ups have been taken over by lenders in the last 18 months), but that’s the premise.

With Teamshares, that isn’t even part of the story – there’s no operating benefit between a sock maker in Michigan, a bakery in Tennessee, and an auto repair shop in Massachusetts. Therefore the argument for multiple arbitrage is about scale, diversification, and the value of the acquisition flywheel. Maybe that’s worth seven turns of EBITDA. I don’t think it is. I think this SPAC transaction is purely to enable further financial engineering, but the “engineering” here is more Hindenburg than Airbus.

Still it isn’t just up to me. While I just might short Teamshares if the SPAC transaction goes through, I also remember the quote attributed to Keynes “The market can stay irrational longer than you can stay solvent”. And if the market shows this level of irrationality, why wouldn’t my friends who have done self-funded searches band together and sell as a platform? Add some slick branding, I’ll join as an M&A guy, and we can get our own seven or eight turns of multiple expansion. What a world.