Q1 was really busy personally (we bought a house and moved, finally!) and professionally (turns out being a CFO is fun but challenging, particularly when you start in the middle of budget season!) but I wanted to get back into the swing of writing about consumer businesses.

Southern California is the perfect place for a couple wellness influencers / entrepreneurs (before that was even really a thing) to come together with a Harvard MBA. And if there’s two other things America loves, it’s Coca-Cola and a re-invention story.

Suja just filed its S-1, which means they’re at least somewhat serious about going public. I first came across the brand maybe 7 years ago, when it was both growing nicely and burning cash. At that point, its manufacturing site was both unique and underperforming, illustrating that getting brand, product development and operations humming at the same time in a food business is hard but lucrative. They’ve also cracked the code on unit economics in a way they hadn’t before, and the CFO in me is smiling at the mix shift and what it’s driven. So let’s jump into the bougie end of the refrigerated case.

The Origin Story

Suja was born in San Diego in 2012 from a collision of four very different people. Annie Lawless was a recent Arizona State graduate who dropped out of law school to teach yoga, and had been managing her autoimmune conditions since childhood through a deep appreciation for nutrition and food. She and Eric Ethans, a raw food chef she met at a yoga studio, had started making cold-pressed juice in their apartments and delivering it door-to-door to local customers. This involved buying produce at retail prices and juicing it themselves. I’ve got a picture in my head of what this looked like, and if you’ve been to a farmer’s market in a wealthy area in the last decade, you probably do too. The product was almost certainly good, and the business was almost certainly not scalable or all that profitable.

James Brennan, a San Diego restaurateur and serial entrepreneur, tried the juice and was immediately hooked. He brought in Jeff Church, the founder of NIKA Water, a bottled water brand and social enterprise that donated 100% of its profits to clean water projects globally. Church, a Harvard MBA, former independent PE sponsor, who later had an energy drink venture with one of my least favorite NASCAR drivers, tried the juice, and knew there was something here. He also brought something none of the other three had; knowledge of high-pressure processing, or HPP. HPP kills pathogens without heat, which means you can cold-press juice, bottle it, and give it a shelf life of months, not days. This technique enabled national distribution without compromising the nutritional integrity of the product.

They named the company Suja, Sanskrit for “long, beautiful life,” and launched in May 2012 into 45 Whole Foods locations in Southern California. This was well before the Amazon acquisition of Whole Foods, and while getting into the pre-eminent brand in better-for-you grocery retail is no easy feat, many brands cycle out of those tests and disappear.

The Funding History

What happened next reads more like Silicon Valley in the ZIRP times than the beverage aisle.

In 2013, Boulder Brands Investment Group, the investment fund of the natural foods brand conglomerate that owned Smart Balance and Udi’s Gluten Free bread, put in $8 million at a roughly $100 million valuation. The company was less than a year into commercial sales, but if anyone had pattern recognition on where the puck was headed in emerging food trends, it was Boulder Brands.

Then in January 2014, Alliance Consumer Growth (ACG) came in with another minority round. ACG had a thesis around “2.0 brands” (the next generation brand in an existing category that were healthier / cleaner label, and more premium) and had backed KRAVE Jerky, Shake Shack, and EVOL Foods (which ACG and the other investors had just sold to Boulder Brands in late 2013). ACG and Boulder Brands must’ve had such a pleasant back-and-forth negotiation on EVOL that they decided they wanted to keep seeing each other at Suja board meetings. Revenue had reached ~$18 million in 2013 and was heading toward $40 million in 2014. At this stage, growth is usually driven by increased points of distribution and consumer awareness.

The real inflection point in credibility and valuation came in August 2015, when Coca-Cola invested $90 million for a roughly 30% minority stake, implying a valuation of $300 million for a company that had been selling juice for three years. Goldman Sachs’ growth investing division simultaneously acquired close to 20%, leaving the founders with roughly 25% ownership but the majority of board seats, Boulder with around 5%, and employees and earlier investors with the rest.

The strategic logic for getting the beverage behemoth out of Atlanta involved was access: specifically, the Odwalla refrigerated direct store delivery network. As a fresh product, Suja needed to be shipped and stored in the beverage cooler, and in addition to owning many of the brands in those fridges, Coke and Pepsi control much of the underlying infrastructure. Getting to ride alongside Odwalla and Honest Tea could increase Suja’s retail reach by 50% in 12 months and get them into new channels, such as college campuses and convenience stores, that Suja almost certainly couldn’t access efficiently on their own. The thinking was straightforward for both parties. For Suja – the cold-pressed juice category was growing fast, competitors were watching, and if they didn’t capture the shelf space, someone else would. For Coca-Cola, Odwalla was struggling, as high sugar juice drinks were losing share to alternatives like Suja. Those Odwalla trucks were a lot emptier than they were a few years back, and rather than reposition a lagging brand that was already sub-scale for a Fortune 500 company, Coke figured they’d just put a few bucks behind a brand with momentum and fill the trucks that way.

By 2016, Coca-Cola increased its stake and became the majority owner. The founders had successfully turned a home delivery juice operation into a $300 million EV company in four years. And then things got complicated.

Annie Lawless: (One Of) The Founders Who Left and Built Another Brand

Annie Lawless departed from her day-to-day role at Suja in 2016, around the time Coca-Cola consolidated its majority position. I can’t imagine she, or Eric Ethans (the raw food chef) loved showing up to board meetings and sitting shoulder-to-shoulder with people best known for selling carbonated sugar water. This is probably the right time to mention that she went on to do something remarkably similar in a different category.

After leaving Suja, Annie founded Lawless Beauty, a clean cosmetics brand built on the same founding instinct that produced Suja: her autoimmune conditions also made it difficult for her to use or trust most conventional makeup products. So she built the alternative. The brand launched through Sephora’s “Clean at Sephora” program and has grown into a line of 150 SKUs across more than 2,000 Sephora doors, with a hit in its “Forget the Filler” line. As of mid-2025, Lawless Beauty was delivering double-digit revenue growth while the broader prestige makeup category was essentially flat.

From an investor perspective, Lawless ran the early Suja playbook, but stopped there. She took one round of growth equity funding, remains a controlling shareholder and recently returned as CEO. She’s a CEO with a playbook – find a category where the incumbent product is failing health-conscious consumers, build the clean alternative, and scale it through the retail partners that premium brands most want to be in. And with nearly 200k Instagram followers and a husband who (was born on 3rd base but) has been reasonably successful in business in his own right, with the private jet pics to prove it, Lawless is in her element, she’s also made for this category, thesis, and social media age.

The Coke Era and the Dark Years

The S-1, understandably, does not dwell on ancient history. But it’s the most important part of the story for understanding what PSP bought into in 2021 and what the key levers of the turnaround actually were.

By 2018, Suja had crossed $100 million in revenue, and had built out a major manufacturing site in Oceanside, California. The problem was that the operational infrastructure outran the business’s ability to run it efficiently. The Oceanside facility wasn’t humming – it was built for the future, but was struggling to generate attractive yields from its early lines while also dealing with significant fixed cost absorption issues. Brand and product talent had always been Suja’s strength. The products were genuinely beloved, the marketing was sharp, and consumer loyalty was real. But the operational and financial discipline hadn’t kept pace. The company was reportedly burning nearly $10 million a year while core juice SKU growth was decelerating.

The Coke-era distribution thesis also never fully panned out. Scaling a cold chain nationally through a DSD network is harder and more capital-intensive than Powerpoint makes it look, and the promised expansion in retail reach took longer and was more costly than anticipated. The Odwalla network itself was eventually shut down by Coca-Cola in 2020 as the brand was discontinued entirely, during the period of COVID where supply chain challenges led large companies to narrow assortments to the most important SKUs and products.

Wellness shots, meanwhile, were just beginning to show promise as a category. These 2 ounce concentrated wellness formulations were growing faster than juice, but the Suja strategic pivot hadn’t yet occurred. Bob DeBorde joined as CEO in 2019 to build out the shots business and restore operational discipline, but Coke was increasingly signaling that its better-for-you brand portfolio was a distraction. They’d already moved toward exiting Odwalla, Honest Tea (de-emphasized, and then eventually shut down in 2022) and ZICO (sold back to its founder in early 2021). Suja was next.

The hallway very few people went down in Coca-Cola HQ, circa late 2020?

Paine Schwartz Partners Acquires Suja

On August 23, 2021, Paine Schwartz Partners (“PSP”) acquired a majority stake in Suja. PSP is the largest private equity firm exclusively focused on food and agriculture, with roughly $6.5 billion in AUM and 20-plus years as a firm.

Their two core investment themes are productivity and sustainability in the global food system, and the consumer shift toward health and wellness. Kevin Schwartz, PSP’s CEO, described himself publicly as a “longtime, loyal consumer” of Suja’s products. Either he’s got a real investing-from-personal-experience approach or it’s solid LP pitch framing. Possibly both.

What makes PSP interesting, and the right buyer for an operationally complex business that the most successful beverage company in the world was about to throw in the towel on, is that they’re not a generalist investor that happened to buy a juice company. They have operational experts embedded with portfolio companies, deep cold chain and food manufacturing expertise, and a repeatable playbook for consumer brands that have genuine consumer love but operational and financial challenges. They’ve since deployed the same framework across Promix (supplements), Urban Farmer (specialty dough contract manufacturer), and most recently BetterCo Holdings, a new platform they launched in late 2025 to aggregate earlier-stage better-for-you brands.

Maybe it’s hindsight, but PSP showed some real commitment to the initial founding vision of Suja by bringing in co-founder James Brennan as an operating partner and Suja board member. Interestingly, Brennan founded a separate beauty brand from Lawless called Kopari Beauty, which eventually raised from Catterton. The juice to beauty pipeline is real, and very SoCal. He’s also on the board of BetterCo, so the ties with PSP go beyond Suja.

What Paine Schwartz Actually Did

The thesis / value creation plan at Suja under PSP has four main tenets.

First, fix manufacturing. They inherited an Oceanside site that was too big for the brand (at the time) and not pumping out product efficiently. Over the four years since acquisition, PSP expanded Oceanside by more than 50% while also adding automation to drive line-level efficiency. The S-1 describes a farm-to-bottle timeline of as few as eight days, a 99%+ fill rate at retail, and five HPP units capable of processing roughly 1,500 gallons per hour. Oceanside is now one of the largest vertically integrated cold-pressed beverage facilities in North America.

Second, upgrade the team. Bob DeBorde, already at Suja since 2019, stayed for a few more years. In 2024, PSP recruited Maria Stipp as CEO. Stipp is a 30-year beverage industry veteran with experience at Sapporo and Lagunitas, specifically chosen for her background in operational execution at complex beverage manufacturing businesses.

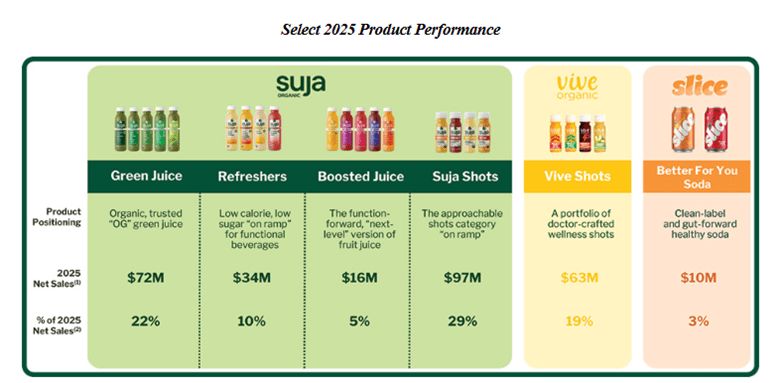

Third, grow the shots business. PSP made a clear strategic bet that shots, and not the 12 and 16 ounce juice bottles that had built the brand, were where the category was going. More on the unit economics of that decision below.

Fourth, M&A. In October 2022, Suja acquired Vive Organic, a wellness shots brand founded in 2015 by Wyatt Taubman, with a doctor-crafted positioning and immunity-focused formulations built around ginger, turmeric, echinacea, and elderberry. Vive had real brand equity including the #1 and #2 SKUs in the wellness shots category, but lacked the sourcing know-how, manufacturing scale, marketing budget, and distribution reach to keep up with consumer demand. Suja identified $14 million in synergies and completed integration in under twelve months, bringing Vive manufacturing in-house at Oceanside.

Together, Suja Organic and Vive Organic now command over 40% of the wellness shots category. Suja Organic holds approximately 47% of the cold-pressed juice category.

The gross margin picture tells the operational story cleanly: even after the ship had been righted in the early years of PSP ownership, margins expanded by 366 basis points from fiscal 2023 to fiscal 2025, reaching 48%, a meaningful improvement for a food manufacturing business, driven by scale, automation, and favorable mix shift toward shots.

The Slice acquisition in May 2024 is the “option value” in the IPO story, with significant potential upside but currently a drag on profitability. Suja/PSP purchased the intellectual property of the better-for-you soda brand originally introduced in the mid 1980s and reformulated it for the Gen Z/Alpha’s. They added prebiotics, probiotics, postbiotics, removed artificial ingredients, and directly targeted the Poppi and Olipop drinker, launching in January 2025.

Slice generated approximately $10 million in net sales in its first full year of operations, but is running at -$26 million Adjusted EBITDA. This is a Silicon Valley P&L for a fizzy drink. Suja would say this is deliberate, as the company is investing heavily in brand awareness, distribution expansion, and trial in the early stages of building what they hope will be a meaningful position in the $35 billion soda category. That Slice EBITDA number is significant enough that it’s dragging total company Adjusted EBITDA sideways even as the core business is accelerating. IPO investors will have to spend the time breaking the core and growth brands apart, but it’s interesting to see a PE firm invest so heavily in a speculative brand late in their hold. Given IPO mechanics, PSP is logically investing for the long term. Even if Suja successfully goes public, it’s highly unlikely PSP will sell many/any shares until at least 6+ months post-IPO, when these brand investments may start to drive growth in Slice. And if not, Suja will likely cut the marketing off and hope the increased profitability boosts the stock price.

Financial Breakdown – Bubbly But Not Popping

The revenue trajectory is genuinely impressive at a time when many food brands are struggling to grow. Net sales grew from $224 million in fiscal 2023 to $259 million in fiscal 2024 to $327 million in fiscal 2025, a 21% CAGR. The Suja Core segment (everything except Slice) grew 23% to $320 million in fiscal 2025, with segment Adjusted EBITDA of $66 million and a 21% EBITDA margin.

Q1 2026 preliminary results, also disclosed in the S-1, show net sales of $103.8–107.1 million — up roughly 21% from the same period last year — and Adjusted EBITDA of $22.9–25.0 million, up approximately 59% year-over-year. Management specifically cited the Suja and Vive Shots as the primary volume driver in Q1 2026, with favorable product mix toward shots also identified as the leading contributor to gross profit improvement.

The Shot Thesis: Why the Little Bottle Might Be the Most Important SKU in the Cooler

Here is where I want to spend a little time, because the unit economics of shots versus juice explain a lot about why this business is getting better as it scales, and why the strategic bets from 5+ years ago are continuing to show up in the financials.

Start with the obvious thing that even I noticed as a PE VP many years ago: a 2 ounce wellness shot retails for somewhere between $3.50 and $5. A 12 or 16 ounce bottle of cold-pressed juice retails for $5–9. On a per-SKU basis, shots generate less revenue per transaction. But on every other dimension that matters to a manufacturer and retailer, they’re superior.

Manufacturing cost: The S-1 states that shots have “lower manufacturing and packaging cost than Suja Single Serve and Suja Multi Serve.” A 2 ounce bottle uses a fraction of the produce volume of a 12 ounce juice, requires smaller, simpler packaging, and goes through the filling lines with considerably less complexity than a full-size juice. When the company says Q1 2026 gross profit improved partly due to “favorable product mix as Suja and Vive Shots have a lower manufacturing and packaging cost,” that’s true both on a $ basis and on a % of revenue basis.

Shelf real estate: A 2 ounce shot takes up a fraction of the linear shelf space of a 12 ounce bottle. Twelve shots occupy less refrigerator real estate than one large juice, and at $4 per unit, the revenue per linear foot of shelf can be competitive with or superior to a larger-format juice that sells less frequently. For a retailer who is trying to squeeze as many dollars out of a refrigerated case, they’re thrilled to see 2 ounce shots that might retail for the same price as a cold brew coffee, iced tea or kombucha, for way less real estate. Remember that Suja isn’t just competing with itself for this space – they’re competing with many other brands and categories, and those other categories generally don’t have a 2 ounce SKU.

Purchase frequency and habit formation: Cold-pressed juice is a more considered purchase than a shot, due to liquid volume and price point. You buy when you’re feeling health-conscious, maybe on the way to the gym, or on a Sunday morning after making some regretful Saturday night decisions involving higher-proof liquids. A 2 ounce shot is more accessible as a daily ritual. The S-1 describes 7% year-over-year growth in occasions per buyer and 6% growth in value per buyer. Over ten years in, Suja is still driving volume growth with its like-for-like customers, in addition to winning new ones.

Category growth: The wellness shots category grew more than 28% in the 52 weeks ending December 2025, outpacing the cold-pressed juice category’s 23% growth. Both of those are awesome in the context of a broader beverage market growing at 3%. While we’re all trying to stay more hydrated, there’s only so many fluids we can drink, and more of those fluids are wellness shots.

Since PSP brought Vive manufacturing in-house, Vive’s sales have grown 50% and SKU velocity has grown more than 96% over two years. That’s what happens when a strong wellness brand gets proper manufacturing and marketing resources, and access to 37,000+ stores.

Stepping Back – Strategic Outlook and the IPO

Suja is one of the great brand stories in better-for-you beverages, with nearly 50% market share in cold-pressed juice and awareness that’s strong and rising fast. But high-end juice at scale is a difficult economic proposition for consumers and household penetration is already 11%, input costs are high and out of Suja’s direct control. The Company is levered and sub-scale for the public markets – there are plenty of PE buyers for $40-60m EBITDA businesses, so the fact PSP isn’t pursuing that path is probably because they’re hoping public markets investors have a different valuation calculator than a larger PE firm.

Slice is a coin flip and could be the reason why we’re excited about this company in three years, or it could be a footnote. Spending $36 million in costs to generate $10 million in net sales in year one is a big bet and financial mismanagement if it continues indefinitely. It’s on a brand with genuine nostalgia and high NPS scores, but those things don’t pay the bills alone. The better-for-you soda category is getting crowded but given the size of the underlying soda category and the lower price point relative to juice, it has more uncapped upside. If Slice works, it could be a bigger brand than Suja; if it doesn’t, it’s an expensive lesson in the difficulty and cost of disrupting legacy soda (which could get even more expensive after PepsiCo spent nearly $2 billion to buy Poppi.

The Suja story has many different flavors: a founder with a personal story, a blitz-scale fundraising run through some big name strategic and financial investors, a pivot in corporate behemoth strategy that imperiled the future of a tail brand, a dark chapter of operational issues, cash burn and slowing growth, a genuine value-added PE investment from a firm that understands the sector, a strategic pivot toward a higher-margin product category that was just beginning to take off, and now a potential IPO.

If you believe wellness shots are becoming a daily habit for a meaningful slice of the American consumer, then you want to take a shot on buying the stock when you can, given it and Vive are the two most-trusted names in the category. As for me – while I think the Company has juice (ha), I’m actually betting the IPO won’t happen. Signaling a willingness to go public is PSP’s tool to keep a potential strategic buyer honest on valuation, but ultimately the brand and category momentum is something another larger food business is going to own.